From Weapons to Wages

Key Takeaways

Foreign Military Sales (FMS) serve as both a national security tool and an economic engine by strengthening U.S. partners while simultaneously channeling billions of dollars back into the U.S.

By leveraging the rising demand for U.S. weapons, FMS can help rebuild the U.S. industrial base and create durable, high-wage manufacturing jobs.

States that proactively invest in defense-ready infrastructure, workforce pipelines, and targeted incentives have a generational opportunity to benefit from the economic growth that will result from this industrial expansion.

Overview

Decades of offshoring of manufacturing jobs have hollowed out the American industrial base, including the Defense Industrial Base (DIB), leaving America’s ability to secure its interests in a degraded state. Between 2000 and 2016, the United States lost nearly five million manufacturing jobs, leaving entire communities deprived of the durable, high-wage work that once anchored them and which formed so much of American life until recent decades. Rebuilding that base is among the most pivotal economic challenges of this moment and a central commitment of the second Trump Administration. What is less widely understood is that one of the most powerful instruments for doing so is already in place, authorized, and is funded by someone other than the American taxpayer. That instrument is FMS.

Foreign Military Sales

FMS is a longstanding tool of American foreign policy that serves as the process for the sale and transfer of American weapons, platforms, systems, or munitions to allies and partners around the world. FMS serves as an avenue for expanding diplomatic relationships while simultaneously protecting the security interests of the United States.

In 2024, the combined value of security assistance under FMS totaled $117.9 billion; of that figure, $96.9 billion, roughly 82%, was paid directly by allies or partners. That is nearly $100 billion in foreign capital flowing into American communities, factories, and supply chains, all while not competing with the domestic procurement budget. There is no other industrial policy lever that combines this scale and funding structure. Put simply, when a partner buys a weapon, such as the F-16, the customer pays the bill, and the work, the wages, and the capacity remain in the U.S.

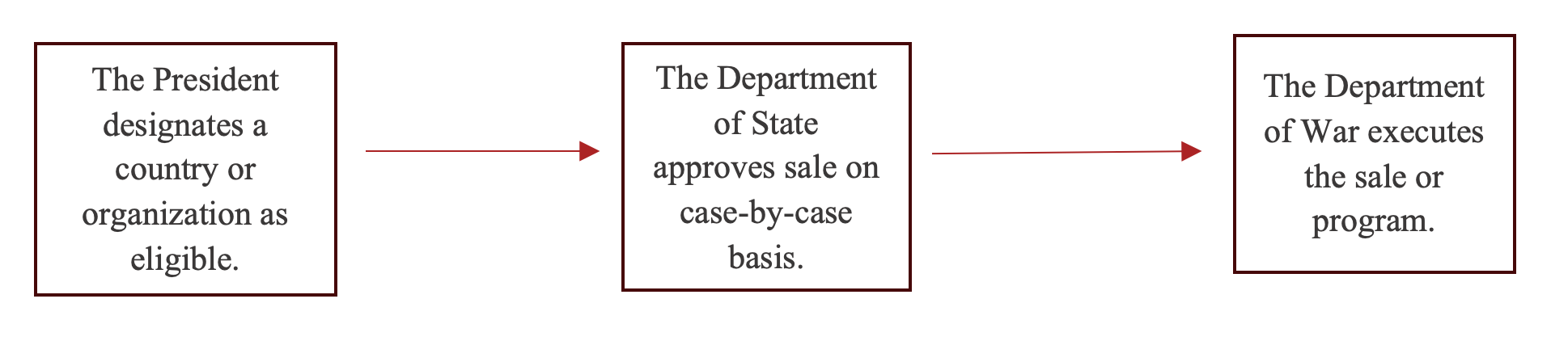

FMS is authorized under Section 3 of the Arms Export Control Act (AECA), which allows the U.S. to sell defense articles and services (such as training) to countries or international organizations that the President identifies as necessary for the security of the United States.

The program serves both diplomatic and security ends: it deepens partnerships, strengthens allied capability, and develops interoperability and weapon standards across coalitions. By supplying our partners with U.S. made weapons, it ensures that allies can operate together with the United States coherently by aligning the weapons, systems, and training. Beyond these ends, the program serves as a mechanism to convert allied demand into domestic manufacturing capacity.

Capital that is received from this program directly supports American communities through existing defense contracts awarded across multiple states. FMS helps sustain the heartland industrial base by supporting manufacturing jobs, suppliers, and production lines that underpin America’s arsenal of freedom.

The Process

The FMS process begins with a foreign partner submitting a request for U.S. defense articles, services, training, or sustainment. Upon approval from the U.S., the customer and the U.S. government enter a Letter of Offer and Acceptance (LOA), a government-to-government agreement under which the foreign customer does not contract directly with a U.S. defense firm. Instead, the U.S. government manages the sale, collects the funds, and uses the Department of War acquisition system to contract with the American defense companies.

Once an FMS case is accepted and funded, the funds enter the U.S. defense contracting system. Companies compete for the contract, and awards are made based on the capability, system, or service required for the case. While larger firms (i.e., Boeing, RTX) often serve as prime contractors who manage the integration and delivery of major platforms or weapon systems, the broader DIB ultimately powers production. A single prime contract pulls in tiers of subcontractors that supply the components, raw materials, software, and specialized services required to build, integrate, and sustain the system.

This process results in a distributed economic footprint. Any given FMS case routinely touches multiple states, congressional districts, and local supplier networks. A significant portion of the work is distributed throughout this supply chain, meaning that FMS supports not only major defense companies but also the heartland communities, factories, and businesses that sustain America’s arsenal of freedom.

AFPI has pulled together data across 17 FMS cases, following the process from the original Defense Security Cooperation Agency (DSCA) notification, through the prime contract award, and into the Federal Subaward Reporting System (FSRS). These chains reach 48 U.S. states at the subcontractor level. Together, the 17 cases represent an estimated $9.3 billion in reported subcontracts across 13,585 individual subaward records. Despite this data not being exhaustive, it demonstrates how FMS contracts reach nearly every state in the United States. As an important caveat, the subcontract data is a floor in its value; across the cases reviewed here, FSRS captures anywhere from zero to 50% of a prime contract's obligated value, with a median of roughly 19%, as the remainder flows through unreported lower supply-chain tiers or is kept by the prime. This means the real distribution of such capital is much wider and underscores the impact this process has on the American industrial base.

Rebuilding the DIB to Reverse Decades of Local Economic Decline

Through Executive Order 14383, “Establishing an America First Arms Transfer Strategy,” President Trump has recognized the opportunity that foreign military sales represent as a single, underutilized lever for rebuilding the broader DIB. At a moment when global demand for American arms is increasing, FMS demand has emerged as a significant instrument within the Administration's economic agenda for rebuilding the American DIB, which decades of offshoring have hollowed out. Since China's World Trade Organization (WTO) accession, the U.S. manufacturing base has eroded sharply, with nearly 5 million manufacturing jobs lost between 2000 and 2016 and entire manufacturing communities decimated across the industrial Midwest and South. While the DIB is not always recognized as a driver of manufacturing expansion, its supply chain sustains a substantial share of America's remaining high-wage industrial employment. As the President actively encourages allied and partner nations to procure American weapons, expanding DIB capacity to meet that demand is essential to translating the elevated FMS demand into economic growth.

the wage premium

A key pillar of the second Trump Administration's economic agenda is getting Americans into good, high-paying jobs by reorienting the American economy toward greater domestic self-reliance to drive the revitalization of manufacturing and the industrial base. The DIB is uniquely positioned to deliver on this pillar, and chief among the reasons is the wage premium attached to jobs across the defense supply chain.

The wage premium associated with DIB expansion is evident not only in the present but on a historical timeline as well. During World War II, the federal government built defense manufacturing plants in counties across the country, often based on wartime considerations rather than on which places were already economically robust, and through new authorities like the Defense Production Act (DPA). American wartime manufacturing of military technology and its overwhelming effect became among the deciding factors in the U.S. victory. A recent study compared counties that received plants with similar counties that did not measure the long-run economic effects of those plants on communities. The authors found that defense plant construction caused a permanent 10% increase in average manufacturing production worker wages in plant counties. Moreover, they found that men born before World War II in those counties earned, on average, $1,200 per year (2.5%) more in adulthood, with the largest gains captured by children of low-income parents. The findings reinforce the long-run case for DIB investment, as the wage premium persisted in plant counties across generations, despite wartime contracts ending.

Today, this trend remains true. Manufacturing wages remain elevated compared to wages in other sectors, with manufacturing workers earning a 10.4% premium over comparable non-manufacturing workers. This is due to several factors, including skill premiums, capital intensity, and the United States’ position as the technological frontier of advanced manufacturing. Defense manufacturers build cutting-edge weapons, and the development of those weapons demands higher-skilled workers, who in turn command higher wages, as documented in a previous AFPI publication.

Beyond the sector-wide premium, the local impact of DIB expansion is even more pronounced in communities anchored in FMS production. Aerospace and Defense (A&D) wages are more than 60% above the local average across these communities, peaking at about 96% in Tarrant County, Texas (home to Fort Worth).[1] Furthermore, it is incredibly encouraging that several of these areas (St. Louis among them) are places that have been identified by Secretary of War Pete Hegseth as central to the economic revitalization of the "Heartland" during his Arsenal of Freedom tour. In areas like Fort Worth, where Lockheed Martin houses its Aeronautics division—producing F-16s and F-35s, both major FMS programs—and employs roughly 19,000 workers, the premium translates into thousands of households earning above the metropolitan area’s average wages. A similar scenario is taking place in St. Louis, where Boeing recently announced that its Defense, Space & Security (BDS) headquarters will move back to, bringing 18,000 high-wage jobs with it. These examples are recent successes for several communities, but the trends can be extrapolated to the broader A&D industry, which supports 2.2 million workers with average labor income of $115,000, roughly 56% above the national average, and generates nearly 1.5% of U.S. GDP in economic value. The second Trump Administration has seized the opportunity to bolster the DIB by pulling the FMS lever in tangible and multi-faceted ways, building on a longstanding conversation about the need for defense manufacturing investment and bolstering the defense and tech ecosystems in such a way that offers a tech future and career progression in 21st-century manufacturing. It serves the national interest to draw talented Americans into the industry and its broader supply chains, which offer durable, high-paying careers.

growth OPPORTUNITIES FOR state and local communities

As FMS volume surges, the economic output it generates increasingly reaches beyond prime contractors themselves. Subcontracting networks, supplier relationships, and capital flows extend into surrounding states and neighboring communities. Whether these communities capture the full benefit depends on how well state and local leaders integrate DIB expansion into their economic development agendas. Beyond the wage premiums established above, three economic indicators matter most. The first is the economic multiplier, which turns each direct DIB job into additional employment across the local economy, resulting in a direct increase in GDP. The second is R&D spillover, where defense investment catalyzes private innovation in host communities. The third is durability, since defense prime contractors and their suppliers tend to expand within communities they have already entered rather than building new facilities elsewhere, which makes the resulting jobs sticky and the benefits compounding. If that trend continues to hold, every relationship a state or locality secures today can accelerate output and investment for the foreseeable future.

Economic Multipliers

DIB expansion delivers both direct and indirect benefits to local communities. The direct effects—new high-paying jobs and an expanded local tax base—are visible immediately. The indirect effects emerge more gradually but are no less consequential. Research using regional variation in defense spending finds that each dollar of defense spending raises local GDP by approximately $1 of additional output, with an additional $0.35 in spillovers to other cities in the same state. Each new manufacturing job is estimated to support 0.8 to 1.6 additional jobs in local non-tradeable sectors, which translates directly into revenue for Main Street businesses. For example, where DIB expansion directly employs welders and engineers, its indirect effects can build out the retail, construction, restaurant, and service economy that turns a contract award into broader economic prosperity.

Research and Development (R&D) Spillover

The multiplier effects above capture the visible economic impact of defense contracts, but a less visible and equally important effect is the spill over into private innovation. Over time, defense firms build an intellectual moat in their host communities that insulates them from brain drain. With skilled workers anchored locally, the investment environment becomes ripe for private capital to follow. Research shows that when defense R&D rises by 10%, privately funded R&D in the same sector rises by roughly 5%, and a one percentage point increase in defense R&D as a share of value added raises annual productivity by roughly 8%. Contrary to popular belief, defense investment does not displace private innovation but instead facilitates follow-on investment. The development of both the internet and GPS can be credited to defense investment, and the first major company in Silicon Valley was Lockheed Martin's Missiles and Space Division. As emerging technology firms continue to usher in a new age of innovation, states that want to spread prosperity through their communities must embrace those frontier companies within their borders.

Durable Jobs and Distributed Benefits

A recent Dallas Federal Reserve paper directly rebutted critics who frame DIB expansion as extractive or transient. It found that the number of business establishments in DIB-receiving counties did not change significantly, meaning the U.S. may not be experiencing a wave of new firms entering local markets to capture contracts. This implies that employment gains in these counties are derived from existing prime contractors and subcontractors expanding, rather than solely from new entrants—though, as the cases below will show, well-anchored new firms like Anduril expand the base rather than displace it. From an economic standpoint, this is favorable. When established firms expand, sunk capital, supplier relationships, and trained workforces are already in place. For defense manufacturing, capital intensity, security clearances, and qualification testing create high barriers to entry, which makes incumbent expansion the primary driver of durable economic impact. The paper validates this effect, finding that prime activity generates large, multi-year expansions rather than transient gains. Furthermore, the reach of these benefits extends beyond the host site into the broader region. The study shows that over 70% of subcontract dollars flow across state lines, and nearly 90% across county lines, meaning that a prime's impact is not confined to a single community. As the cases below show, states that deliberately anchor these relationships convert that reach into durable regional economies.

State Opportunity

The U.S. remains the leader in the development of weapons and military technology around the world, putting the U.S. in a unique position of leverage. Not only does this position the U.S. well in terms of security, but it also provides an opportunity for economic growth within the United States. The recent focus from the Trump Administration on revitalizing the DIB establishes a foundation for long-term industrial growth, investment, and job creation across the country. States possess a unique opportunity to establish incentives that attract defense-related industries, strengthen local manufacturing ecosystems, secure domestic supply chains, and position their communities to help power America’s arsenal. In what follows, we provide a deeper look at the current situation in four states and what our data says regarding the relationship between FMS contracts and job creation.

Ohio (Anduril)

One of the clearest cases of a state taking advantage of the opportunities that come from the DIB has been in Ohio, where the state-level bidding environment has attracted one of the most promising new defense companies, Anduril. Ohio utilizes a unique nonprofit organization, JobsOhio, to bolster the state’s economic development.

One of the functions of JobsOhio is to establish economic incentives to attract new corporations into the state. The nonprofit announced a layered bid offer for Anduril that amounts to a total of $832 million, the most money ever awarded to any company coming to the state of Ohio. This funding includes $310 million in grant funding over the next ten years, tax credits worth $452 million over 30 years, and an additional $70 million for a taxiway at Rickenbacker International Airport.

The funding is planned to go toward Anduril's upcoming manufacturing operation in Pickaway County, the site of Anduril’s Arsenal-1 factory. In exchange for this funding, Anduril is expected to maintain continued investments through 2055 and create 4,008 new jobs, which would amount to more than $530 million in new payroll and more than $910.5 million in capital investment. Arsenal-1 is expected to be operational by 2035, with average salaries around $132,305 a year. This deal and accompanying incentives are said to be finalized sometime in the summer of 2026.

Missouri (Boeing)

St. Louis County has long been the home of significant Boeing manufacturing operations, which continue to create substantial economic opportunity for the local community and the state more broadly. This impact is set to be even more significant with the announcement of a new 1 million-square-foot manufacturing facility, costing Boeing $1.8 billion.

In exchange for this new facility, St. Louis County agreed to give Boeing a 50% abatement on real and personal property taxes for any new investment, which translates to an estimated $155 million in revenue over 10 years. Boeing, in turn, guaranteed an additional 500 high-paying jobs to serve as a return on this investment. Beyond straight cash incentives, St. Louis County has consistently worked to strengthen the relationship with Boeing over time by investing in the infrastructure and campuses surrounding the Lambert International Airport, which had been vacant for decades.

What made this move by St. Louis County even more impressive was that it happened before the Air Force awarded Boeing the contract for the next-generation fighter, the F-47. This program provides further opportunities for the local community—where Boeing already employs over 16,000 people—by providing continued job security and future growth.

This case demonstrates how economic incentives can foster a sustained relationship with a company that offers continued growth, while also highlighting the significance of new contracts.

Arkansas (Highland Industrial Park)

Arkansas is quietly making itself into one of the most concentrated defense manufacturing corridors in the country at the Highland Industrial Park in East Camden. The bustling industrial park now hosts names such as Lockheed Martin, RTX, Rafael, L3Harris, General Dynamics, and Aerojet Rocketdyne.

This project was not done overnight; it was an intentional, systematic process led by the state over a decade. The state has been able to maintain the Highland Industrial Park as a state-controlled asset, enabling more expedited and unified development and making such a large-scale project possible. Governor Sarah Huckabee Sanders also developed multinational relationships, which resulted in a joint venture between U.S.-based Raytheon and Israel-based Rafael Protection Systems (R2S). The joint venture secured a $1.25 billion contract to produce interceptor missiles. This massive contract was awarded just weeks after the two companies invested roughly $63 million in a new facility in the region.

Arkansas has also solidified itself as a central piece in FMS, with the Air Force's selection of Ebbing Air National Guard Base in Fort Smith as the new home for the FMS Pilot Training Center. This project is expected to bring in roughly 900 military members, along with their families, as well as sustained capital as FMS contracts continue.

The case in Arkansas shows the benefits of taking on state-controlled projects to build up a large industrial corridor to attract these companies. The munitions being built here, solid rocket motors, are also very hard to relocate, effectively leaving Arkansas with a large chunk of these defense assets that will compound for decades. Governor Huckabee Sanders also demonstrates how a governor can take on the onus in building international relationships that can play a major role in securing contracts that further propel the demand and manufacturing for these projects.

Alabama (Redstone Arsenal)

Alabama is focusing on Huntsville and Madison County, intending to regain the State’s industrial prominence. This has manifested in decades of investment in the U.S. Army Redstone Arsenal, a 38,000-acre federal installation that houses 65 tenant organizations. The installation generates $36.2 billion annually for Alabama’s economy, providing 90,000 jobs. One of the biggest wins for the region was the Trump administration’s announcement that the U.S. Space Command would relocate around 1,400 jobs to Redstone Arsenal over the next five years. In another major win, the U.S. Army’s $9.8 billion PAC-3 Patriot missile contract was awarded to Redstone, making it the largest missile contract ever received by the arsenal.

The City of Huntsville took a unique approach in utilizing a milestone-triggered incentive structure rather than the use of up-front grants. Two announcements made in August demonstrate this strategy. Performance Drone Works (PDW) opened a $9.1 million 87,720 square foot unmanned aerial systems (UAS) facility that will create 525 new jobs with an average salary of $105,000, with the project being backed by $500,000 from the City of Huntsville if PDW hits its hiring benchmarks. Parsons Corporation will also be expanding its current facilities, committing $5 million in investment and 198 new jobs with an average salary of more than $100,000. Huntsville will provide up to $237,600 to Parsons as it hits these benchmarks. Further catalyzing, Cummings Research Park launched a DefenseTech Accelerator in 2024, leveraging the Innovate Alabama Tax Credit, which permits in-state taxpayers to redirect 50% of their state tax liability toward local defense-tech startups.

Redstone Arsenal demonstrates how a state can leverage new approaches to revitalize industrial sites that long served as the backbone of America’s military strength. Strategies such as milestone-triggered incentive structures can support the industry while offering guarantees of job growth in local communities. As these facilities continue to grow, the opportunity for taxpayers to contribute to local defense and tech startups will further fuel this growth by supporting newer, innovative companies that often serve as subcontractors, thereby strengthening these industries from the bottom up.

What can be learned

The states landing new DIB facilities in 2025-2026 are not the ones with the largest checkbooks. They are the states that have invested, for a decade or more, in the capabilities that make them low-risk choices: executive engagement, targeted incentive structures, pre-permitted sites, industrial power capacity, specialized workforce pipelines, and durable deal structures. The size of the subsidy is what closes the deal, but it is the steps a state takes beforehand that open the door. With President Trump's continued strive to return the U.S. to a manufacturing powerhouse and his continued stride to drive up demand via FMS, the opportunity is generational, and it's not too late for states to get a piece.

[1] Source: U.S. Bureau of Labor Statistics, Quarterly Census of Employment and Wages (QCEW), 2024 annual averages, private ownership. Aerospace reflects NAICS 3364 (aerospace product and parts manufacturing) for Madison County, AL and Tarrant County, TX, and NAICS 336413 (other aircraft parts and auxiliary equipment manufacturing) for St. Louis County, MO, where 3364 is suppressed; 336413 is a narrower segment that understates St. Louis aerospace pay. Baselines are all private industries in each county. Average annual pay is total wages divided by average annual employment across all covered jobs; it is a mean, not a typical worker's earnings. Because these codes cover manufacturing only, the figures exclude defense engineering and R&D and thus understate the full premium.