529 Plan Conformity across the states: A Reform Agenda After the One Big Beautiful Bill

Key Takeaways

« 529 plans are tax-advantaged savings accounts through which families invest for qualified education expenses.

« Federal legislation in 2017 and 2025 expanded 529 plans beyond college savings, allowing families to use funds for a broad range of K-12 expenses—representing a meaningful expansion of education freedom.

« Fourteen states and D.C. have not fully conformed their laws to one or both sets of federal changes, leaving families in those jurisdictions exposed to state tax penalties on withdrawals that are federally tax-free.

« States should conform 529 statutes to federal law, strengthen contribution incentives, and remove barriers that prevent residents from fully using these robust savings vehicles.

Introduction

529 education savings plans, also known as qualified tuition plans, are tax-advantaged accounts in which families invest after-tax dollars in mutual funds, index funds, and age-based portfolios offered by plan administrators under contract with state governments. Earnings grow free from federal income tax, and withdrawals remain tax-free when used for qualified education expenses. Established under Section 529 of the Internal Revenue Code, these plans were originally designed to help families save and pay for postsecondary education but have expanded significantly in the past decade to include tuition and other expenses in K-12 education—making them dramatically more attractive vehicles for education freedom. When parents save for college, their children benefit through reduced educational debt (Elliott et al., 2014), and even small levels of school-designated savings strongly predict postsecondary enrollment and graduation (Briscese et al., 2025; Elliott, 2013).

In 2025, American families held a combined $576.7 billion in assets in 529 plans (Investment Company Institute, 2026; Credit Karma, 2025). While all states except for Wyoming sponsor a 529 program (Education Commission of the States, 2020), state tax treatment varies considerably, particularly with respect to K-12 usage.

Recent Congressional legislation broadened the definition of qualified educational expenses, but state conformity to these federal changes is uneven. Some states fully exclude K-12 expenses, while others identify tuition as the only eligible K-12 category. This may cause confusion in non-conforming states, leaving residents at risk of state tax penalties should they withdraw funds for expenses that qualify under federal law but not under their own state’s code.

Existing research on 529 policy examines how states have responded to federal changes (Burke & Butcher, 2017; Mann, 2019; Trinidad & Johnson, 2025), but this research report advances on prior work in several dimensions. First, it is the most current analysis available, published after states have had sufficient time to respond to federal changes to 529 plans included in the One Big Beautiful Bill Act. Second, it provides the most thorough documentation of state law assembled in one place, with direct citations to statutory text, administrative rules, and plan manager guidance for each state’s conformity determination. Finally, this report examines state-level tax incentives for 529 contributions and advances policy recommendations to expand education freedom through 529 plans.

Background

History of 529 Plans

529 plans originated as state prepaid tuition programs, through which parents purchased future enrollment at participating colleges or universities. Michigan launched the first such program in 1986, which prompted litigation over its federal tax treatment (Michigan Education Trust Act, 1986, Sec. 390.1421-390.1442). In State of Michigan v. United States, the Sixth Circuit ultimately ruled that these tuition programs were exempt from federal income tax (State of Michigan and Michigan Education Trust v. United States of America, 1995), laying the groundwork for future federal policy.

In 1996, Congress codified 529 plans through the Small Business Job Protection Act (H.R. 3448, 1996). Subsequent legislation expanded allowable expenses to include room, board, and college tuition (H.R. 2014, 1997), though earnings accumulated only on a tax-deferred basis with qualified withdrawals subject to federal tax. By 2000, 30 states had created their own 529 programs (College Savings Plans Network, n.d.).

The 2001 Economic Growth and Tax Relief Reconciliation Act permitted tax-free withdrawals for qualified expenses (H.R. 1836, 2001), and the Pension Protection Act of 2006 made tax-free withdrawals permanent (H.R. 4, 2006). Later 529 expansions included technology-related expenses such as computers, peripheral equipment, and internet access (H.R. 2029, 2015).

Expansion to K-12

The 2017 Tax Cuts and Jobs Act (TCJA) marked the first significant expansion of 529 plans beyond higher education, amending the definition of qualified education expense to include up to $10,000 in annual tuition expenses at K-12 public, private, or religious schools (H.R. 1, 2017). This landmark legislation expanded educational freedom by providing parents with another option for educating their children in nonpublic elementary and secondary schools. Two years later, the SECURE Act added student loan repayments and certified apprenticeships as allowable expenses (H.R. 1865, 2020). SECURE 2.0 passed Congress in 2022, permitting up to $35,000 in 529 funds to be rolled over into Roth IRAs for retirement savings (H.R. 2617, 2022).

Most recently, the One Big Beautiful Bill Act (H.R. 1, 2025) doubled the amount families can annually withdraw—from $10,000 to $20,000—and extended allowable K-12 withdrawals to include homeschooling expenses. The complete list of qualified K-12 educational expenses, as of this writing, is:

- Tuition;

- Curriculum and curricular materials;

- Books or other instructional materials;

- Online educational materials;

- Tuition for tutoring or educational classes outside of the home, including at a tutoring facility;

- Fees for a nationally standardized norm-referenced achievement test, an advanced placement examination, or any examination related to college or university admission;

- Fees for dual enrollment in an institution of higher education; and

- Educational therapies for students with disabilities provided by a licensed or accredited practitioner or provider, including occupational, behavioral, physical, and speech-language therapies.

These expansions have transformed 529 plans from college savings vehicles into comprehensive tools for financing education from kindergarten through postsecondary, thereby broadening the options available to families at every stage of a child’s academic career.

As federal progress has accelerated, so too has the cost of inaction at the state level. Every jurisdiction that fails to conform or build on these changes leaves its residents with less educational freedom than Congress intended.

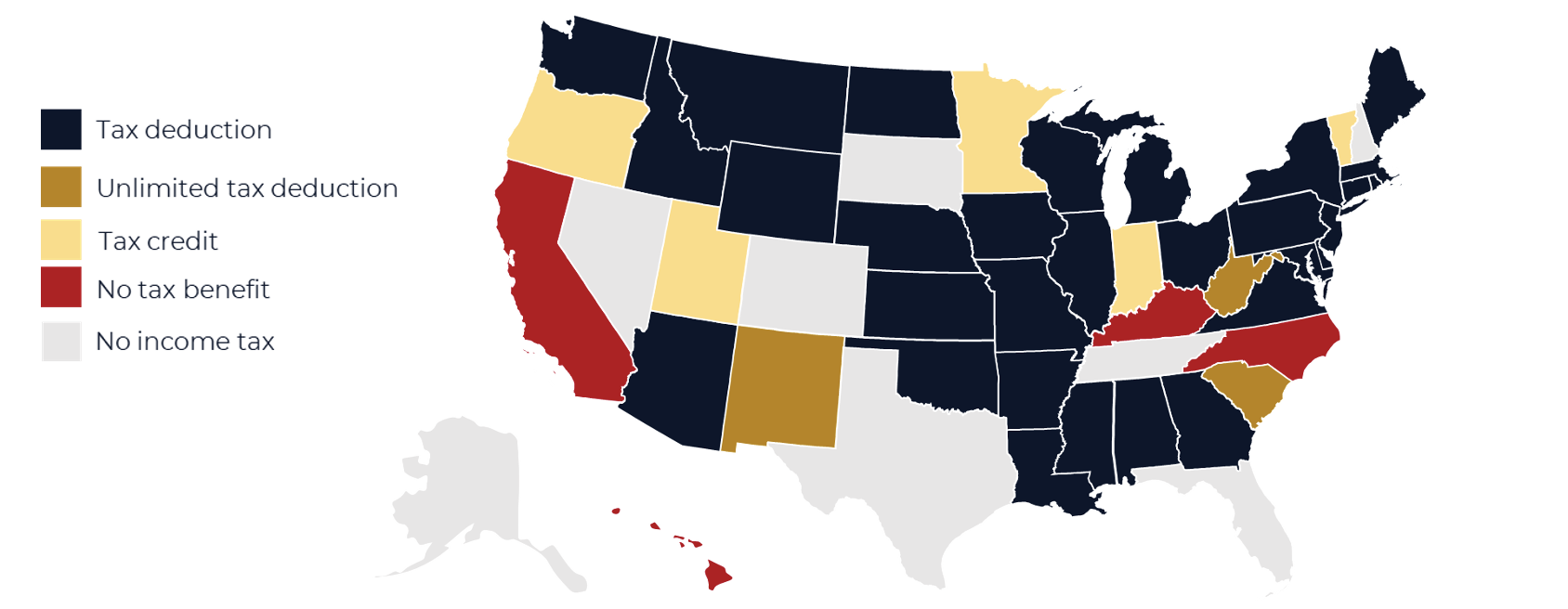

State Tax Incentives

Most states offer tax incentives for contributions to a 529 plan, though the amount and form of benefits vary considerably. Three states—New Mexico, South Carolina, and West Virginia—permit unlimited state income tax deductions for contributions, subject to federal gift tax rules for contributions exceeding $19,000 per donor (or $38,000 for married couples filing jointly) in a single year, unless contributors elect five-year gift tax averaging. Most states allow a more limited state tax deduction, and several others offer limited nonrefundable credits against state taxes. (See Figure 1 below, and Appendix A for a full list of tax benefits in each state, including sources.)

Figure 1 State Tax Benefits

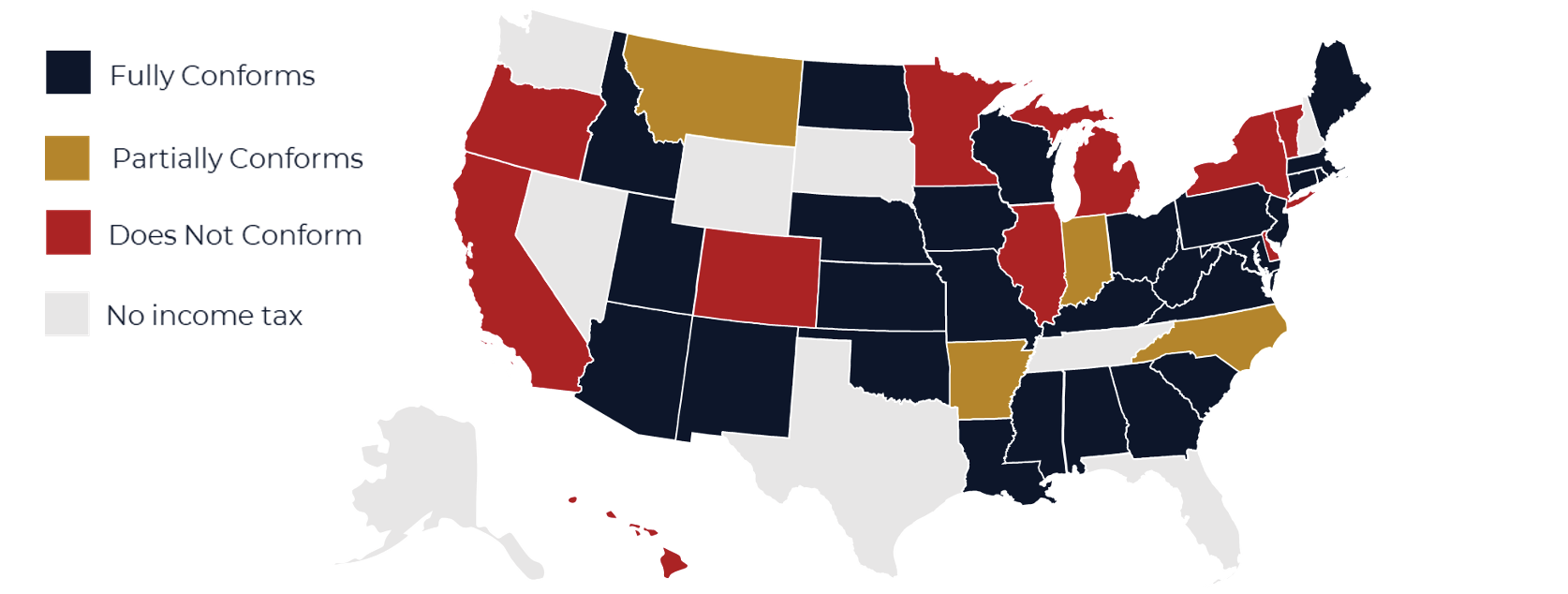

State Conformity to Federal Law

Federal expansions of the qualified expense definition, which occurred in 2017 and 2025, do not automatically bind states to make the same changes. Families in non-conforming states may therefore face state tax liability on withdrawals that are federally tax-free, creating an invisible compliance trap for account holders. This report analyzes statutory text, administrative rules, and 529 plan manager guidance to categorize states into one of two groups: (1) fully conforming states that adopted both the 2017 TCJA and 2025 OBBBA changes through automatic statutory conformity or explicit legislative amendment; and (2) partially or non-conforming states that restrict education freedom by continuing to limit 529 use to higher education. (See Figure 2 below and Appendix B for complete details on state conforming status, including sources.)

Figure 2 State Conformity to Federal Law

Fully Conforming States

The following 27 states conform to the 2017 and 2025 changes, either through automatic statutory conformity or by manually updating statutes to explicitly identify new qualified expenses: Alabama, Arizona, Connecticut, Georgia, Idaho, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Mississippi, Missouri, Nebraska, New Jersey, New Mexico, North Dakota, Ohio, Oklahoma, Pennsylvania, Rhode Island, South Carolina, Utah, Virginia, West Virginia, and Wisconsin.

- Automatic statutory conformity. Many states reference federal definitions “as amended,” automatically incorporating future Congressional changes without needing new state legislation. This approach eliminates statutory lag and reduces administrative uncertainty for families.

- Example: Mississippi Code Section 37-155-105 defines an “institution of higher education” as “an eligible educational institution as defined in Section 529 of the Internal Revenue Code of 1986, as amended, or any other applicable federal law” and a “qualified higher education expense” as “any higher education expense, as defined in Section 529 of the Internal Revenue Code of 1986, as amended, or other applicable federal law.”

- Example: Louisiana Statute Section 17:3100.1 holds that “any requirement of this Chapter determined to be more restrictive than the requirements of the federal Internal Revenue Code as applicable to a qualified tuition program may be modified to conform with code requirements by the Louisiana Tuition Trust Authority in accordance with the Administrative Procedure Act.” This mechanism grants a state agency authority to conform to federal law even where the statutory definitions appear more restrictive on their face.

- Explicit statutory enumeration of new eligible expenses. Other states amend their laws to explicitly include eligible expenses that were identified by Congress in 2017 or 2025. This approach is workable but risks non-conformity unless the statute is regularly updated or also includes automatic conformity language.

- Example: Arizona Statute Section 15-1871 states that “qualified higher education expenses… include tuition…to enroll in or attend an elementary or secondary public, private or religious school pursuant to section 529 of the internal revenue code.”

- Example: Iowa Code Section 12D.1 defines “qualified education expenses” as “the same as ‘qualified higher education expenses’ as defined in section 529(e)(3) of the Internal Revenue Code, and shall include elementary and secondary school expenses for tuition described in section 529(c)(7) of the Internal Revenue Code, subject to the limitations imposed by section 529(e)(3)(A) of the Internal Revenue Code.”

Partially and Nonconforming States

States that partially or entirely do not conform to federal law generally do so through one of four ways: static references to federal code as of a fixed date; broad agency discretion to define qualified expenses; a discrepancy between statutory language and agency/plan manager interpretation; or explicit statutory exclusion of K-12 expenses.

The following states partially conform to federal law, meaning they have adopted the 2017 changes, allowing funds from 529 accounts to be used for K-12 tuition, but not the 2025 changes that include K-12 expenses beyond tuition: Arkansas, District of Columbia, Indiana, Montana, and North Carolina.

The following states do not conform to federal law, meaning they have not adopted the 2017 or 2025 changes, only allowing 529 plans to be used for higher education expenses and effectively disallowing K-12 expenses: California, Colorado, Delaware, Hawaii, Illinois, Michigan, Minnesota, New York, Oregon, and Vermont.

- Static reference to federal code as of a fixed date. These states cross-reference federal definitions with an “as of [DATE]” clause that identifies a date prior to the 2017 or 2025 Congressional amendments.

- Example: Arkansas Code Section 6-84-103 defines “qualified higher education expenses” as “tuition and other permitted expenses as set forth in 26 U.S.C. § 529, as in effect on January 1, 2024, for the enrollment or attendance of a designated beneficiary.” Because the amendments to federal law that include additional K-12 expenses were passed in 2025, these changes are not yet recognized by Arkansas, as confirmed by their 529 plan manager (Bright Future Direct Plan, 2025).

- Example: North Carolina conforms to the “Internal Revenue Code as enacted as of January 1, 2023, including any provisions enacted as of that date that become effective either before or after that date,” according to the North Carolina General Statutes Section 105-228.90. Accordingly, the state conforms to the TCJA amendments but not those included in OBBBA (College for North Carolina, n.d.).

- Broad agency discretion to define qualified expenses. Here, statutory text explicitly directs state agencies to determine what constitutes a qualified expense.

- Example: California Education Code Section 69980 defines “qualified higher education expenses” as “the expenses of attendance at an institution of higher education… if, as determined by the board, the amendment is consistent with the purposes of this article, and as determined and certified by the institution of higher education in the same manner as prescribed in Title IV of the Higher Education Act of 1965 (20 U.S.C. Sec.1087l1, as amended).” California allows its ScholarShare Investment Board to determine if amended federal definitions are consistent with the purposes of state law, which is a considerable amount of discretion granted by the legislature to unelected civil servants.

- Discrepancy between statute and state agency or plan manager. In these states, the statutory text would seem to conform with federal law, but the relevant agency or plan manager does not appear to be following it.

- Example: While Indiana Code Section 21-9-2 defines “qualified higher education expenses” as those “set forth in Section 529 of the Internal Revenue Code,” its Department of Revenue asserts that “distributions made from an Indiana 529 Plan that are used to pay for K-12 expenses other than tuition at an in-state school are not qualified withdrawals,” and specifically identifies expenses added by the OBBBA as “disallowed expenses” (Gully, 2026).

- Example: Montana permits 529 withdrawals for K-12 tuition but not the additional K-12 expenses made allowable by OBBBA. According to Montana’s 529 plan manager, the state’s Department of Revenue has not yet determined if K-12 or credentialing expenses are considered qualified for Montana state income tax purposes (Achieve Montana, n.d.). Montana Code Section 15-62-103 defines an “education expense” as “expenses for tuition, fees, books, supplies, equipment required for an education program, principal or interest on any qualified education loan, and any other typical education expense associated with an education program up to the maximum amount allowable under section 529 of the Internal Revenue Code, 26 U.S.C. 529, as amended,” which suggests that all K-12 expenses should be allowable.

- Statutory exclusion of K-12 expenses. These states require that qualified expenses be made at institutions of higher education, thereby excluding tax-free withdrawals for K-12 learning.

- Example: Hawaii Statute Section 235-2.4(ii) excludes all K-12 expenses by stating that “Section 529 (with respect to qualified tuition programs) shall be operative for the purposes of this chapter, except that sections 529(c)(6), 529(c)(7) and 529(e)(3)(A)(iii) shall not be operative.” Section 529(c)(7) is the section of federal law that refers to K-12 expenses.

- Example: Illinois only includes higher education as qualified expenses, with its statute defining an “eligible educational institution” as “public and private colleges, junior colleges, graduate schools, and certain vocational institutions that are described in Section 1001 of the Higher Education Resource and Student Assistance Chapter of Title 20 of the United States Code (20 U.S.C. 1001) and that are eligible to participate in Department of Education student aid programs,” according to Illinois Code Chapter 15 Section 505/16.5.

- Example: Oregon Statute Section 316.680 states that “if a taxpayer makes a withdrawal from a savings network account for higher education… to pay expenses in connection with enrollment or attendance at an elementary or secondary school, the amount of the withdrawal that is attributable to contributions that were subtracted from federal taxable income" is added to the Oregon taxable income base, subjecting those withdrawals to state income tax.

Policy Recommendations

1. States should adopt automatic conformity to federal law.

States with an income tax should reference 26 U.S. Code § 529 “as amended” rather than explicitly defining a then-current list of qualified expenses. Mississippi and Connecticut are good models to follow. When state adoption lags federal enactment, families who made good-faith withdrawals during the intervening period should be protected by retroactive safe harbor provisions, so they do not incur tax penalties. Using static language that incorporates federal definitions with an “as of [DATE]” clause, like Arkansas and North Carolina, requires states to pass new bills to restore parity every time the federal code is amended and should be avoided.

Moreover, state legislatures should correct conflicts between state statutes and agency guidance where agencies are interpreting 529 law contrary to statutory text. For example, Indiana and Montana have statutory language that under plain reading appear to conform to federal law, but revenue agencies issued guidance or otherwise interpret state law to exclude certain K-12 expenses.

2. States should expand tax incentives for contributions to 529 plans.

States with an income tax should increase both the value of their 529 contribution incentives and the contribution amounts eligible for those benefits. More generous state tax incentives will encourage families to save for medium- and longer-term education expenses while also reducing reliance on debt to finance postsecondary education (Elliott et al., 2014).

States that offer no contribution incentive—California, Hawaii, Kentucky, and North Carolina among them—should establish a deduction or credit. Those with smaller annual deduction caps should consider the model established by New Mexico, South Carolina, and West Virginia, each of which permits an unlimited deduction against state income.

The choice between deductions and credits depends on policy goals. Deductions are likely to produce the largest aggregate amounts of educational saving, but the overall amounts will be skewed toward higher income families. Credits distribute the incentive more evenly across the income spectrum and are better suited to broadening participation.

3. States should extend tax benefits to contributions made into out-of-state 529 plans.

Most states restrict tax deductions or credits to contributions made into their own plan, limiting investment options and prioritizing state revenue over educational savings. Families enrolled in underperforming in-state plans should retain tax benefits when choosing a more attractive plan in another state. The only states that currently offer this benefit are Arizona, Arkansas, Kansas, Maine, Minnesota, Missouri, Montana, Ohio, and Pennsylvania (J.P. Morgan Asset Management, 2026).

4. States should provide tax incentives for employers who contribute to or match contributions to employees’ 529 accounts.

Employer-sponsored 529 contributions extend savings to families who might not otherwise set money aside for educational purposes. Arkansas, Colorado, and Pennsylvania currently allow employers to receive a business tax deduction of up to $500 per employee for matching contributions to a 529 account—a model for other states to consider (Arkansas Brighter Future 529, n.d.; Colorado Department of Revenue, n.d.; Commonwealth of Pennsylvania, n.d.-b).

5. States with Education Savings Accounts should allow families to roll unspent balances into 529 accounts.

States that operate Education Savings Account (ESA) programs (Paul, 2026) should permit families to roll unspent ESA balances into 529 accounts without state tax consequences, rather than reverting those dollars to the general fund. Federal law does not yet provide a dedicated rollover mechanism for this type of transfer, meaning ESA balances moved into a 529 account could be treated as a new contribution and count against annual gift tax exclusion limits. At the federal level, Congress should establish a dedicated rollover mechanism that allows ESA balances to transfer into a 529 account after a student graduates from high school. Otherwise, families face a perverse incentive to spend down ESA funds rather than save for postsecondary costs.

6. Congress should expand 529 expenses to include first-home down payments.

For families whose children do not pursue postsecondary education, 529 savings should not sit stranded, particularly given that many institutions of higher education have failed to deliver the economic returns implied by their tuition costs. Homeownership remains one of the most reliable pathways to long-term wealth creation. Accordingly, Congress should permit 529 beneficiaries to apply their savings toward a down payment on a first home, preserving the value of disciplined saving regardless of a beneficiary’s decision to enroll in college (Faulkender, Homan & Takeda, 2026).

7. The Treasury Department should issue guidance requiring each state’s 529 plan manager to disclose discrepancies between federally-qualified expenses and state-qualified expenses.

This guidance would not by itself force states to conform to federal law, but it would limit potential tax penalties on residents who are unclear about whether they may use 529 plans for K-12 expenses without incurring state tax penalties, and it would provide a clear roadmap for state legislators to rectify non-conforming statutes.

Conclusion

529 plans have evolved from a narrow college savings vehicle into a versatile tool for financing education from kindergarten through postsecondary education. The TCJA and OBBBA together extended this flexibility to K-12 education, an expansion that parents in most states can now access. But 14 states and the District of Columbia have not fully conformed to one or both sets of federal changes, leaving families in those jurisdictions exposed to state tax penalties on withdrawals that are federally tax-free.

The recommendations in this report outline the path forward: states should conform their statutes, strengthen contribution incentives, and eliminate barriers to using 529s—all of which will put more parents in a position to better customize education to meet the unique needs of each child.

Appendix A. State Tax Benefits for 529 Contributions

| State | Type of Tax Benefit | State Tax Benefit | Source |

|---|---|---|---|

| Alabama | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) | Alabama Administrative Code Rule 810-3-15-.27 |

| Alaska | - | No income tax | - |

| Arizona | Tax Deduction | Up to $2,000 per beneficiary (Single), $4,000 (Joint) Tax Parity State |

Arizona Statutes Section 43-1022.19 |

| Arkansas | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) Tax Parity State |

Arkansas Code Section 6-84-111 |

| California | - | No tax benefit | - |

| Colorado | Tax Deduction | Up to $26,200 per beneficiary (Single), $39,200 (Joint) | Colorado Revised Statute Section 39-22-104 |

| Connecticut | Tax Deduction | Up to $5,000 (Single), $10,000 (Joint) | Connecticut Statute Ch. 229 Section 12-701a |

| Delaware | Tax Deduction | Can deduct up to $1,000 (Single); $2,000 (Joint) | 30 Delaware Section 1106b |

| District of Columbia | Tax Deduction | Can deduct up to $4,000 (single); $8,000 (joint) | DC College Savings Plan |

| Florida | - | No income tax | - |

| Georgia | Tax Deduction | Up to $4,000 per beneficiary (Single), and $8,000 (Joint) | Code of Georgia Section 48-7-27 |

| Hawaii | - | No tax benefit | - |

| Idaho | Tax Deduction | Up to $6,000 single, $12,000 joint | Idaho Code Section 63-3022 |

| Illinois | Tax Deduction | Up to $10,000 (Single), $20,000 (Joint) | 35 Illinois Code Statute Section 5/203a (2)(D-20) |

| Indiana | Tax Credit | 20% income tax credit Maximum tax credit amount of $750 (single)/$1,500 (Joint) |

Indiana Code Section 6-3-3-12k |

| Iowa | Tax Deduction | Up to $6,100 per beneficiary, up to 4 beneficiaries ($24,400); adjusted annually for inflation | Iowa 529 Plan Manager |

| Kansas | Tax Deduction | Up to $3,000 per beneficiary (Single), $6,000 (Jointly) | Kansas Statutes Section 79-32,117(c)(xv) |

| Kentucky | - | No tax benefit | - |

| Louisiana | Tax Deduction | Up to $2,400 per beneficiary (Single), $4,800 (Joint) | Louisiana 529 Plan Manager |

| Maine | Tax Deduction | Up to $1,000 per beneficiary Tax parity state; income cap of $100,000 (single) or $200,000 (Joint) |

36 Maine Revised Statutes Section 5122.2(YY) |

| Maryland | Tax Deduction | Up to $2,500 (Single), $5,000 (Joint) | Maryland Code Section 10-208 |

| Massachusetts | Tax Deduction | Up to $1,000 (Single), $2,000 (Joint) | Massachusetts 529 Plan Manager |

| Michigan | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) Tax Parity State |

Michigan Code of Laws Section 206.30.1(D)(t) |

| Minnesota | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) Tax Parity State |

Minnesota Statutes Section 290.0132, Subdivision 23 |

| Mississippi | Tax Deduction | Up to $10,000 (Single), $20,000 (Joint) | Mississippi Code Section 37-155-113 |

| Missouri | Tax Deduction | Up to $8,000 (Single), $16,000 (Joint) | Missouri Code Section 166.435 |

| Montana | Tax Deduction | Up to $4,500 (Single), $9,000 (Joint) Tax Parity State |

Montana Code Section 15-30-2120 |

| Nebraska | Tax Deduction | Up to $5,000 (single), $10,000 (joint) | Nebraska Code Section 77-2716(8)(c) |

| Nevada | - | No income tax | - |

| New Hampshire | - | No income tax | - |

| New Jersey | Tax Deduction | Up to $10,000; Income cap of $200,000 |

New Jersey Statutes Section 54A:3-12 |

| New Mexico | Tax Deduction | Unlimited | New Mexico Statutes Section 7-2-32 |

| New York | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) | New York 529 Plan Manager |

| North Carolina | - | No tax benefit | - |

| North Dakota | Tax Deduction | Up to $5,000 (Single), and $10,000 (Joint) | North Dakota Code Section 57-38-30.3 (2)(m) |

| Ohio | Tax Deduction | Up to $4,000 per beneficiary Tax Parity State |

Ohio Revised Code Section 5747.70 |

| Oklahoma | Tax Deduction | Up to $10,000 (Single), $20,000 (Joint) | Oklahoma Administrative Code Section 710:50-15.66 |

| Oregon | Tax Credit | Up to $190 (Single), $380 (Joint) Income phaseout for those making $200,000 |

Oregon Revised Statutes 315.650 |

| Pennsylvania | Tax Deduction | Up to $19,000 per beneficiary (Single); $38,000 (Joint) Tax Parity State |

Pennsylvania 529 Plan Manager |

| Rhode Island | Tax Deduction | Up to $500 (Single); $1000 (Joint) | Rhode Island Code Section 44-30-12 (c)(4) |

| South Carolina | Tax Deduction | Unlimited | South Carolina Code Section 59-2-80 |

| South Dakota | - | No income tax | - |

| Tennessee | - | No income tax | - |

| Texas | - | No income tax | - |

| Utah | Tax Credit | Up to $115.20 per beneficiary (Single); $230.40 (Joint) through credit | Utah 529 Plan Manager |

| Vermont | Tax Credit | Up to $250 per beneficiary (Single); $500 (Joint) through tax credit | 32 Vermont Statutes Section 5825 |

| Virginia | Tax Deduction | Up to $4,000 per account | Virginia Code Section 58.1-322.03 |

| Washington | - | No income tax | - |

| West Virginia | Tax Deduction | Unlimited | West Virginia 529 Plan Manager |

| Wisconsin | Tax Deduction | Up to $5,280 per beneficiary | Wisconsin Statute Section 71.05 (6)(b) (32a) |

| Wyoming | - | No income tax & No 529 plan | - |

Appendix B. State Conformity Status

Resources